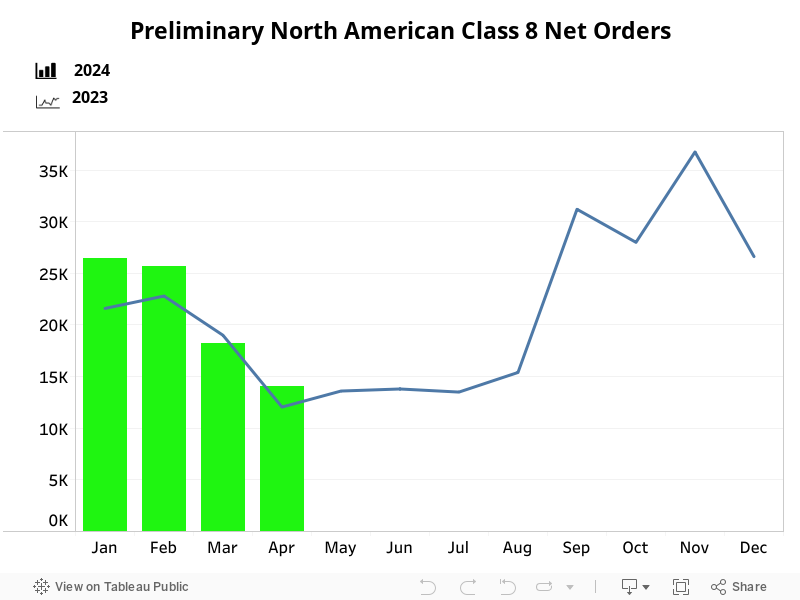

Preliminary North American Class 8 Net Orders for April at 14,000 Units

FTR reported that Class 8 preliminary net orders for April came in at 14,000 units, down 28% from March but up 12.5% y/y. Class 8 orders for the past 12 months total 267,700 units.

Similar to February and March activity, April orders were consistent with the recent demand trend and are in line with seasonal expectations. The levels seen over the first quarter of 2024 mostly quelled concerns of a rapid decline in demand, and the market is performing slightly above replacement-level orders. After maintaining an average level of around 25,000 units over the previous three months, orders have continued to slow at a seasonally typical rate, averaging 20,000 units in the last three months.

OEMs continue to fill build slots at a healthy rate. Although most OEMs saw declining orders, some saw small increases.