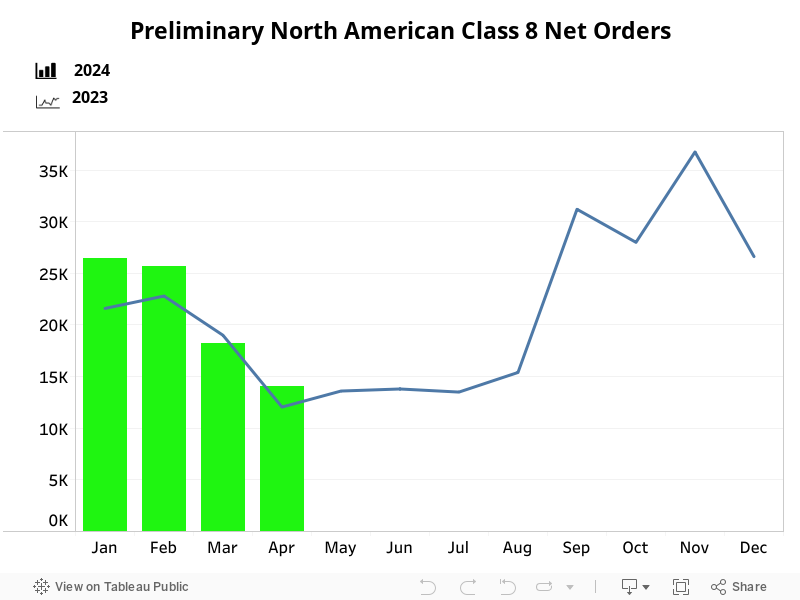

Preliminary North American Class 8 Net Orders for March at 18,200 Units

FTR reported that Class 8 preliminary net orders for March came in at 18,200 units, down 34% from February and 4% below March 2023. Orders for the past 12 months have totaled 264,800 units.

Like February’s activity, March orders are consistent with the recent demand trend and are in line with seasonal expectations. After maintaining an average level of around 27,000 units for the last three months, orders appear to be slowing at a seasonally typical rate. Build slots continue to be filled at a healthy rate. With March orders comparable to the March 2023 level, the market is still performing at a solid level.