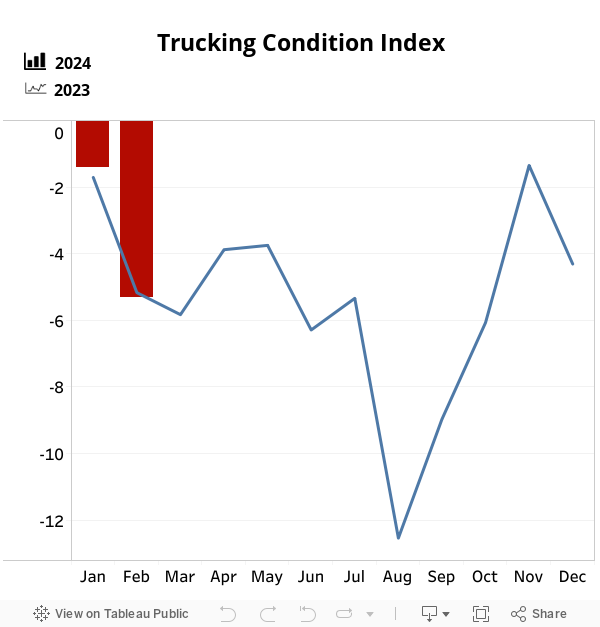

FTR’s Trucking Conditions Index Falls in February Mostly Due to Fuel Costs

FTR’s Trucking Conditions Index for February fell to -5.31 from January’s reading of -1.41. A sharp increase in diesel prices was the principal factor in the deterioration in market conditions for carriers. With the recent increase in crude prices, fuel costs could remain a drag on the TCI in the near term, but freight market dynamics likely will move gradually toward a less challenging environment for carriers.