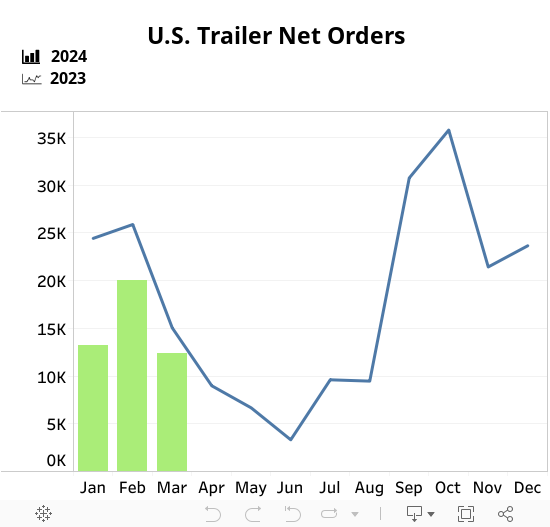

U.S. Trailer Net Orders Fell in March to 12,313 Units

FTR reports that March trailer orders fell 7,659 from February (-38% m/m) to a total of 12,313 units. Orders were down 18% y/y and 25% below the average for the last 12 months.

Trailer production increased by less than 1% m/m in March to 23,505 units. Production was down 21% y/y. This build number is in line with the average production level seen over the past three years.